Amputation Injury Costs: Prosthetics & Compensation Guide

Over 5.6 million Americans currently live with limb loss, and approximately 465,000 new amputations occur each year. While the immediate trauma of amputation is devastating, the long-term financial burden often catches victims and families off guard. Lifetime prosthetic costs frequently exceed $500,000 for above-knee amputations, with initial prosthetic legs ranging from $10,000 to $70,000 and requiring complete replacement every three to five years.

The causes are diverse: 57% of amputations relate to diabetes complications, 40% to vascular disease, and a significant portion result from workplace accidents and vehicle crashes. Most amputees remain unaware of the multiple compensation sources available to help manage these staggering costs. Understanding the true financial scope is essential for securing adequate settlements or benefits that cover not just immediate expenses but decades of prosthetic care.

Understanding Initial Amputation Costs

Before exploring long-term prosthetic expenses, it's essential to understand the immediate financial impact of amputation surgery and hospitalization.

For uninsured patients, initial amputation surgery costs between $20,000 and $60,000, including surgeon fees, facility charges, anesthesia, and medical supplies. However, surgery represents just the beginning. Two-year costs average $91,106 when including hospitalization, rehabilitation, outpatient visits, physical therapy, and the first prosthetic device.

Physical therapy sessions range from $50 to $350 per session, while occupational therapy costs $50 to $400 per session—and patients typically require multiple sessions over months. Pediatric leg amputations incur particularly high costs, with mean hospital charges reaching $120,275 and length of stay averaging 18.5 days.

Even with insurance coverage, out-of-pocket costs for the first 24 months reach at least $90,000. These initial expenses represent only a fraction of lifetime financial obligations, making it critical to calculate total long-term costs when negotiating settlements or applying for benefits.

Prosthetics Cost Breakdown by Type and Technology

While initial surgery costs are substantial, the ongoing expense of prosthetic devices represents the largest long-term financial burden for amputation victims.

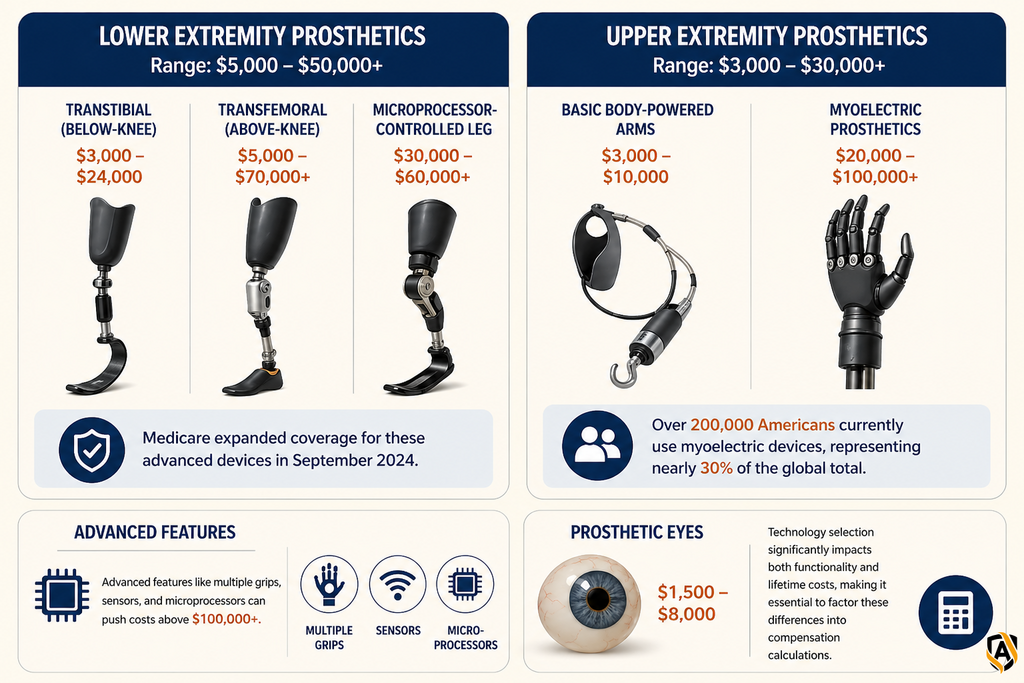

Lower extremity prosthetics range from $5,000 to $50,000 depending on amputation level. Transtibial (below-knee) prosthetics cost $3,000 to $24,000, while transfemoral (above-knee) prosthetics range from $5,000 to $70,000. Microprocessor-controlled legs, which provide more natural movement and stability, cost $30,000 to $60,000. Medicare expanded coverage for these advanced devices in September 2024.

Upper extremity prosthetics range from $3,000 to $30,000. Basic body-powered arms cost $3,000 to $10,000, while myoelectric prosthetics—which use muscle signals for precise movement—range from $20,000 to $100,000 or more. Over 200,000 Americans currently use myoelectric devices, representing nearly 30% of the global total.

Advanced features like multiple grips, sensors, and microprocessors can push costs above $100,000. Prosthetic eyes cost $1,500 to $8,000. Technology selection significantly impacts both functionality and lifetime costs, making it essential to factor these differences into compensation calculations.

Long-Term Financial Impact: Replacement, Maintenance, and Lifetime Costs

The price tags on prosthetic devices tell only part of the story—the recurring nature of replacement and maintenance costs creates lifetime financial obligations.

Prosthetics require complete replacement every three to five years regardless of quality or initial cost. Even the most expensive prosthetic limbs are built to withstand only this amount of wear and tear. Manufacturers cease repairs at the six-year end-of-service lifetime, after which devices are no longer repairable.

Annual maintenance adds substantial costs. Supplies including liners, socks, gloves, and donning materials must be replaced annually and account for 5% to 10% of the complete prosthesis cost. Osseointegrated prosthesis maintenance averages $2,626 per year, while replacement parts can cost thousands more annually. Regular check-ups are required every six to twelve months.

Children face even more frequent replacements. A child with a prosthetic limb needs a new device annually until age five, every two years from ages five to twelve, and every three years from ages twelve to twenty-one. These recurring expenses compound over decades, with pediatric prosthetics costing $5,000 to $50,000 each time.

Insurance Coverage Options: Medicare, Medicaid, and Private Insurance

Understanding lifetime prosthetic costs makes clear why insurance coverage is critical—but also reveals significant gaps that compensation claims must address.

For 2025, Medicare Part B charges a $185 monthly premium and requires a $257 annual deductible. After meeting the deductible, beneficiaries pay 20% coinsurance for external prosthetics. Prosthetics must be obtained from Medicare-enrolled suppliers, and some states require prior authorization for specific prosthetic codes (L5856, L5857, L5858, L5973, L5980, and L5987).

Medicaid coverage operates as an optional benefit, not federally mandated. While all fifty states offer prosthetic support, coverage varies significantly by state. Some states like Washington impose specific replacement schedules, limiting socket replacements to one per twelve-month period per limb. Most states cover copayments, but eligibility requirements and benefit levels differ substantially.

Private insurance typically requires 10% to 50% coinsurance. Durable Medical Equipment like prosthetics faces strict pre-authorization requirements. Plans deny approximately 6% of initial requests, often claiming prosthetics aren't "medically necessary" or are "experimental"—even for decades-old technology like microprocessor knees. However, 82% of denials are reversed on appeal with proper documentation.

Workers' Compensation and Disability Benefits

While health insurance covers some prosthetic costs, work-related amputation victims may access additional benefits through workers' compensation and disability programs.

Workers' compensation covers medical bills and lost wages for workplace injuries. Permanent partial disability (PPD) represents the largest benefit available for limb loss. Benefits follow state-specific schedules based on body parts—for example, Connecticut provides 36 weeks of PPD benefits for losing the first finger.

Permanent total disability (PTD) applies when workers lose or lose use of both hands, arms, feet, legs, or eyes in any combination. PTD pays two-thirds of average weekly wages for life for those who cannot return to work. Between 2015 and 2022, more than 26,200 workplace injuries resulted in amputation, with manufacturing (375.98 per 100,000 workers) and utilities (277.21 per 100,000 workers) representing the highest-risk industries.

Social Security Disability Insurance (SSDI) pays up to $3,822 monthly, though the average benefit is $1,500. Supplemental Security Income (SSI) pays up to $943 monthly. Amputations must be expected to last at least twelve months to qualify under Blue Book Listing 1.20.

Personal Injury Compensation: Settlements and Damages

For amputations caused by third-party negligence, personal injury claims offer the most comprehensive compensation pathway to cover lifetime prosthetic costs.

Settlements range from $200,000 to several million dollars depending on specific case factors. There is no single "average" due to the unique circumstances of each injury. Notable settlements include $9.95 million for a twenty-eight-year-old with traumatic above-the-knee amputation (the largest known result in New York State history), $9.75 million for amputation of both hands and lower legs due to failure to diagnose sepsis (California record), and $3 million for a construction worker who lost his leg in a scaffolding collapse.

Compensation includes economic damages—medical bills, lost wages, and future expenses for medical care, rehabilitation, and prosthetics—and non-economic damages covering pain, suffering, and reduced quality of life. Settlement values vary based on amputation level (thumb amputations typically receive higher compensation than other fingers due to functionality), age, profession, long-term impact on life, the at-fault party's insurance limits, and comparative negligence rules.

Life care plans prepared by certified nurses or rehabilitation specialists are essential. These documents map all anticipated medical needs for the injured person's lifetime, projecting costs of prosthetic replacements every three to five years, ongoing therapy, medical check-ups, medications, and necessary home assistance. Most states impose a one to three-year statute of limitations for filing personal injury claims, making timely legal consultation critical.

Decision Framework: Comparing Coverage Options and Maximizing Benefits

With multiple compensation sources available, injury victims need a strategic framework to identify which benefits apply to their specific situation and how to maximize total recovery.

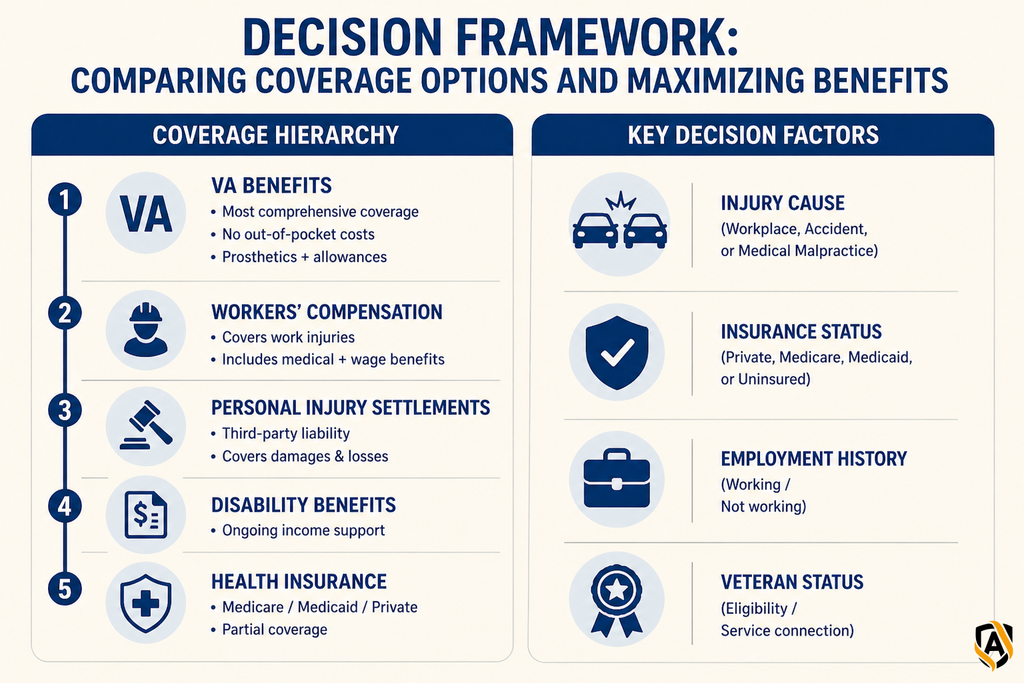

Coverage follows a hierarchy based on injury circumstances. Veterans Affairs benefits provide the most comprehensive coverage with no out-of-pocket costs for most eligible veterans, prosthetics regardless of service connection, clothing allowances, home improvement benefits up to $6,800, and special monthly compensation. The VA operates over 140 amputation care sites nationwide.

Workers' compensation covers work-related injuries, while personal injury settlements address third-party negligence. Disability benefits provide ongoing income support. Medicare, Medicaid, and private insurance offer partial coverage but leave significant gaps.

Key decision factors include injury cause (workplace, vehicle accident, or medical malpractice), insurance status, employment history, and veteran status. Multiple sources often apply simultaneously—for example, workers' compensation plus a third-party liability claim, or disability benefits combined with a personal injury settlement. Understanding how these sources interact maximizes total compensation while avoiding benefit coordination pitfalls.

Taking Action to Secure Your Financial Future

Understanding the compensation landscape is just the first step—taking timely action to pursue all available benefits is essential to securing the resources needed for lifetime prosthetic care.

Lifetime prosthetic costs exceeding $500,000 require a comprehensive compensation strategy. Initial insurance determinations or settlement offers rarely account for full lifetime expenses, often focusing only on immediate medical bills. Multiple compensation sources may apply to a single case, making professional evaluation essential.

Life care plans are critical for calculating true damages and demonstrating to insurance companies, employers, or courts why substantial compensation is necessary. Time is of the essence: most states impose one to three-year statutes of limitations for personal injury claims. Missing these deadlines permanently forfeits your right to compensation, regardless of injury severity or financial need. Contact a qualified personal injury attorney immediately to evaluate your case and maximize available benefits before time runs out.

Frequently Asked Questions

How much does a prosthetic leg cost, and how often does it need replacement?

Prosthetic leg costs vary significantly by amputation level and technology. Transtibial (below-knee) prosthetics cost $3,000 to $24,000, while transfemoral (above-knee) prosthetics range from $5,000 to $70,000. Advanced microprocessor-controlled prosthetics cost $30,000 to $60,000.

Regardless of quality or initial cost, prosthetics require complete replacement every three to five years. Manufacturers cease repairs after six years, making replacement mandatory. Annual maintenance supplies add 5% to 10% of the prosthesis cost. Lifetime costs for above-knee amputations often exceed $500,000 when factoring in multiple replacements, maintenance, physical therapy, and medical appointments over decades.

Does Medicare or insurance cover prosthetic limbs?

Medicare Part B covers external prosthetics with 20% coinsurance after meeting the $257 annual deductible (2025 rates). The monthly premium is $185. Medicare expanded coverage for microprocessor-controlled knees in September 2024, but prior authorization is required for certain prosthetic codes.

Medicaid coverage varies by state, as prosthetics are an optional benefit rather than federally mandated. All fifty states offer some level of support, but replacement schedules, copayment coverage, and eligibility requirements differ significantly. Private insurance typically requires 10% to 50% coinsurance and strict pre-authorization. Approximately 6% of prior authorization requests are initially denied, but 82% are reversed on appeal with proper documentation.

What compensation can I receive for a workplace amputation injury?

Workplace amputation injuries qualify for workers' compensation benefits including medical bill coverage and lost wage replacement. Permanent partial disability (PPD) represents the largest benefit, with amounts determined by state-specific schedules based on the body part lost. Benefits vary significantly—Connecticut provides 36 weeks of PPD for losing the first finger, while other states have different formulas.

If you lose or lose use of both hands, arms, feet, legs, or eyes in any combination, you may qualify for permanent total disability (PTD), which pays two-thirds of your average weekly wages for life. Additionally, if a third party (not your employer) caused the accident, you can pursue a separate personal injury claim beyond workers' compensation. OSHA reported over 26,200 workplace amputations between 2015 and 2022, with manufacturing and utilities industries showing the highest injury rates.

How much is an amputation injury settlement worth?

Amputation settlements range from $200,000 to several million dollars, with no fixed average due to the unique circumstances of each case. Record settlements include $9.95 million for a traumatic above-the-knee amputation (New York State record) and $9.75 million for bilateral hand and leg amputations due to misdiagnosed sepsis (California record).

Settlements include economic damages (medical costs, lost wages, future prosthetic expenses) and non-economic damages (pain, suffering, reduced quality of life). Factors affecting value include amputation level, age, profession, long-term impact, and the at-fault party's insurance policy limits. Thumb amputations typically receive higher compensation than other fingers due to greater functional loss. A comprehensive life care plan documenting lifetime prosthetic replacement costs every three to five years is essential for maximizing settlement value.

What is a life care plan and why do I need one?

A life care plan is a comprehensive document prepared by a certified nurse or rehabilitation specialist that maps all anticipated medical and personal needs for the remainder of an injured person's life. For amputation victims, it projects the costs of prosthetic replacements every three to five years, ongoing physical and occupational therapy, regular medical check-ups, medications, and necessary home assistance or modifications.

Life care plans are essential for personal injury claims because they demonstrate the true cost of amputation extends far beyond initial medical bills. Typical amputation life care plans show $500,000 or more in lifetime costs. Without this comprehensive documentation, insurance adjusters and defense attorneys often undervalue claims by focusing only on immediate expenses. Life care plans provide credible, professionally prepared evidence of future financial needs, significantly strengthening settlement negotiations or trial presentations.

Need Legal Help?

Contact our experienced Austin personal injury attorneys for a free consultation.