What to Do When the Insurance Company Says Your Car Is a Total Loss in Texas

If your insurance company tells you that your car is a total loss, it can feel overwhelming. This article explains what a total loss means in Texas, how the process usually works, and what options people often have when they disagree with the insurance value. Everything here is general information to help you feel more prepared.

What “Total Loss” Means in Texas

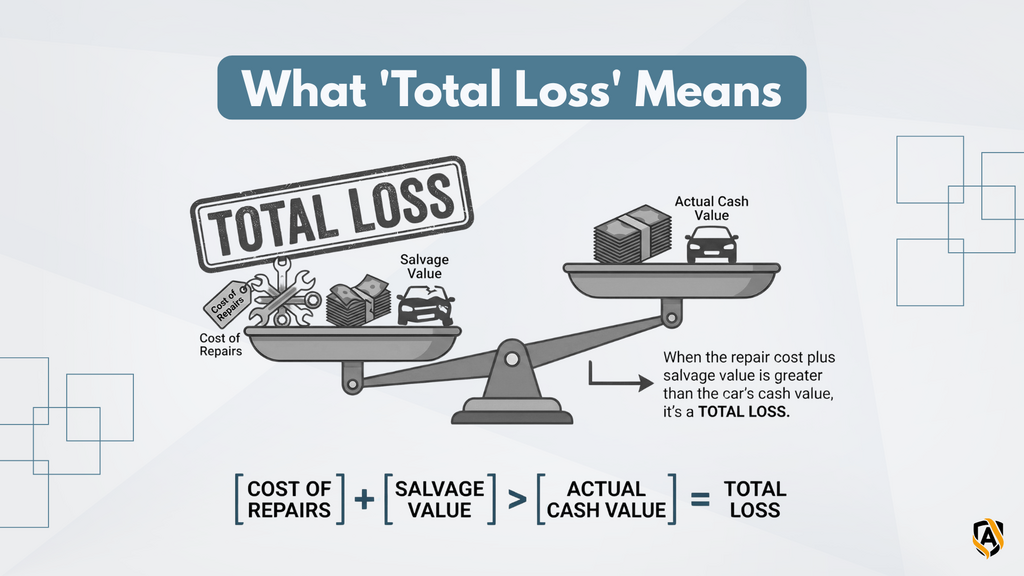

In plain English, a car is considered a total loss when the cost to fix it is more than what the insurance company says the car is worth. Texas uses a formula called the Texas total loss formula. The insurer compares the cost of repairing the car plus the salvage value to the car’s market value. If the numbers do not make sense financially, they call it a total loss.

A few key points

Actual cash value means what your car was worth right before the accident. Insurers look at age, mileage, condition, options, and local market prices.

Salvage value means what the damaged car could sell for at a salvage auction.

The company is not deciding whether the car can be repaired. They are deciding whether it makes financial sense for them to repair it.

What Usually Happens After the Total Loss Decision

Once the company says your vehicle is a total loss, here are the usual steps.

The adjuster gives you a written offer stating the value of your car.

The insurer takes possession of the vehicle if you accept the offer, unless you choose to keep it.

Your loan or lease payoff is sent to your lender first if you still owe money.

You receive the remainder, if any, after the lender is paid.

If you keep the car, the insurer will deduct the salvage value from your payout, and the Texas title will usually become a salvage title. That can affect registration and future insurance.

How the Insurance Company Calculates Your Car’s Value

Insurance companies often use third party valuation tools. They look at local sales of similar cars, condition, mileage, and options. You have the right to ask for the valuation report.

Things to check carefully

Mileage listed correctly

Features or options listed correctly

Whether similar cars used in the report are truly comparable

Maintenance records or upgrades that may support a higher value

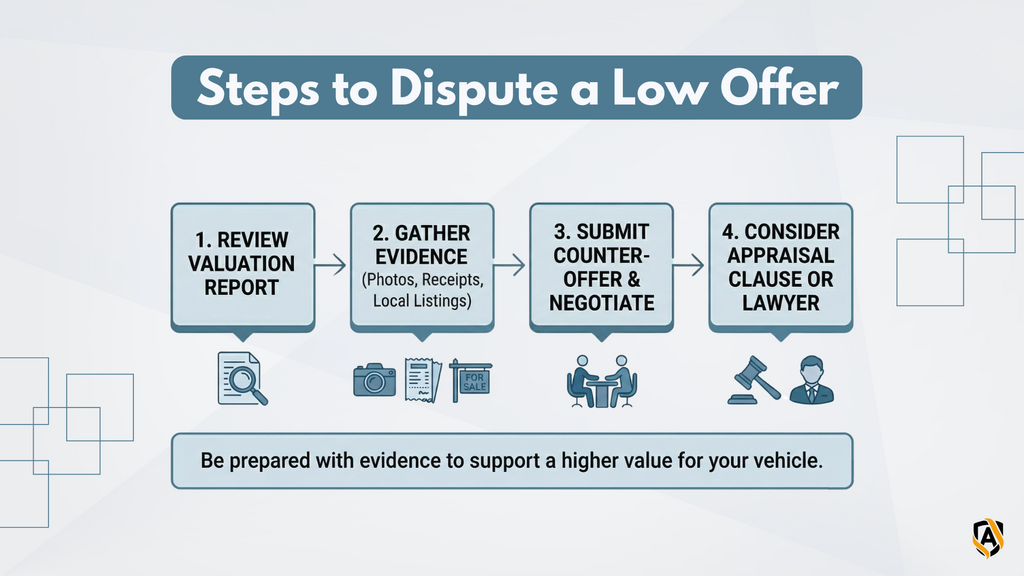

What to Do If You Think the Offer Is Too Low

It is common for people to feel the first offer is not enough. You can ask for a review or submit evidence of a higher value.

Helpful steps

Gather local listings of similar cars in similar condition.

Provide photos, repair records, or upgrade receipts.

Ask the insurer to explain any difference between your research and their valuation.

Stay calm and keep communication in writing when possible.

If you still cannot agree, you can sometimes use the appraisal clause in your policy. The appraisal clause is a process where you pick an appraiser, the company picks an appraiser, and the two appraisers choose a third person. They work together to set the value. This is usually used when there is a real disagreement about the car’s worth.

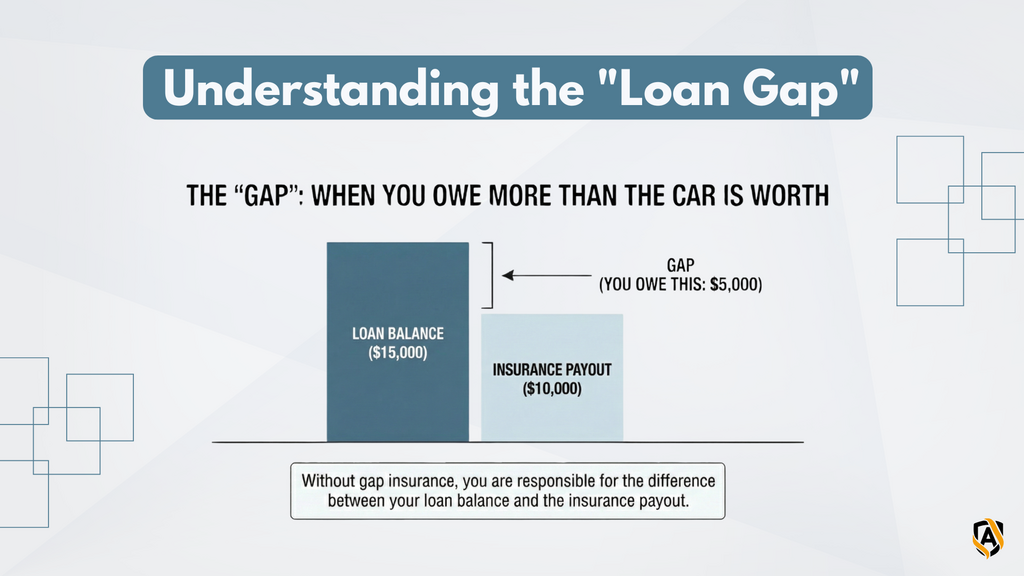

Handling a Total Loss When You Still Owe Money

If you owe more on your loan than the car’s value, you may end up with a balance due. This is called being upside down. Gap insurance is a type of coverage that can help pay the difference, but not everyone has it. If you do not have gap coverage, you may need to work out payment arrangements with your lender.

Common Mistakes to Avoid

Accepting an offer without reviewing the valuation report

Assuming you must accept the first offer

Forgetting to remove license plates and personal items before the car is taken

Not contacting your lender quickly if you still owe on the vehicle

When You Should Consider Talking to a Texas Lawyer

It can be helpful to talk with a lawyer if

You were injured, and the claim is more complex

There is a dispute about who caused the accident

The insurance company refuses to negotiate

You think the insurer acted in bad faith by delaying or undervaluing your claim

A lawyer can explain your rights under Texas law and help you understand whether additional steps make sense.

Final Thoughts

A total loss decision can feel frustrating, but understanding the process can help you make clear choices. Review the valuation report, gather your own evidence if needed, and do not be afraid to ask questions. If your claim becomes complicated or involves injuries, speaking with a licensed attorney can help you understand your options.

This article is for general educational purposes only and is not legal advice. Laws change, and how they apply can depend on your specific situation. Talk to a licensed attorney in your state and in Texas if your issue is in Texas for advice about your particular case.

For over 25 years, Aaron has fought for justice on behalf of Austin's injured. He is committed to standing up to insurance companies and winning for clients across Central Texas.