.png)

Who Pays Your Medical Bills After an Austin Crash? (It’s Not Always the At-Fault Driver)

There is a massive misconception about car accidents that we have to correct almost every day.

You are sitting in the ER at Dell Seton or St. David’s. You are hurt. You know the crash wasn't your faul, the other guy ran the red light on Lamar.

So, when the intake nurse asks for your insurance card, you hesitate.

So, when the intake nurse asks for your insurance card, you hesitate.

You think, "Why should I give them my insurance? The other driver caused this. Send the bill to him."

Do not do that.

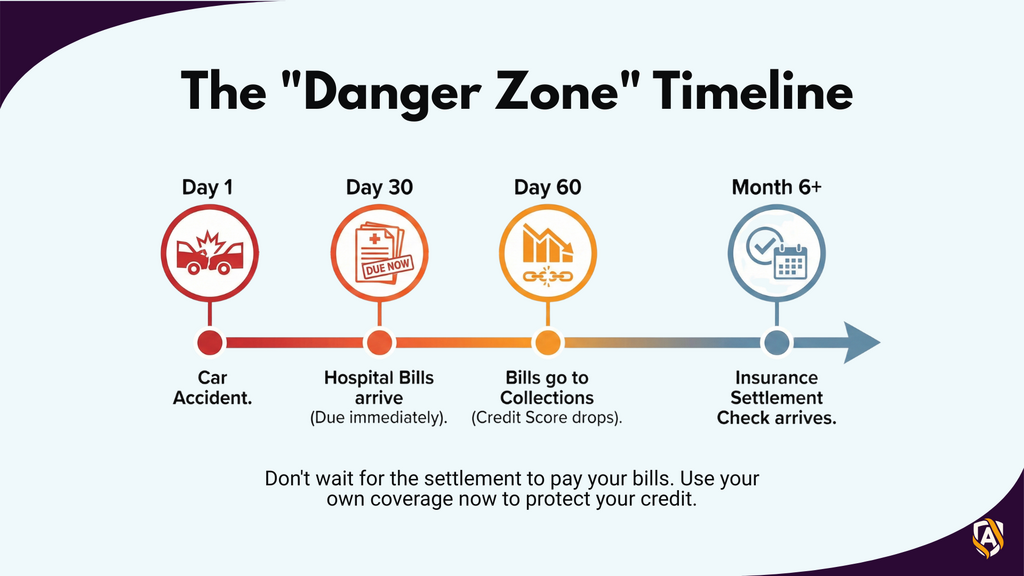

If you wait for the at-fault driver’s insurance company to pay your medical bills as they arrive, you will ruin your credit score.

Insurance settlements happen at the end of the case, which could be six months or a year from now. The hospital wants its money now.

Insurance settlements happen at the end of the case, which could be six months or a year from now. The hospital wants its money now.

Here is the strategic way to handle medical bills in Texas without going broke while you wait for your settlement.

The First Line of Defense: PIP (Personal Injury Protection)

Check your own auto insurance policy. Right now.

In Texas, insurance companies are required by law to offer you Personal Injury Protection (PIP). It usually covers $2,500, $5,000, or sometimes $10,000 in medical bills.

Here is the kicker: It is "No-Fault" money.

It doesn't matter if you caused the wreck or if they did. It doesn't matter if the other driver is uninsured. If you have PIP, your own car insurance pays your doctors directly, up to the limit.

Why people miss this: Many people think using their own insurance will raise their rates. Generally, using PIP for a crash that wasn't your fault does not skyrocket your premiums. It is money you have already paid for. Use it.

Note: If your insurance agent says you don’t have PIP, ask to see the rejection form. In Texas, you must reject PIP in writing. If they can’t produce that signature, they owe you the coverage.

The "Subrogation" Trap (Using Health Insurance)

Once your PIP runs out (or if you don’t have it), you should absolutely use your private health insurance (Blue Cross, Aetna, United, etc.).

"But wait," you ask. "If my health insurance pays, does the other driver get off scot-free?"

No. This brings us to a legal headache called Subrogation.

Here is how it works:

- Your health insurance pays the $50,000 ER bill (often at a discounted rate).

- We sue the other driver and get a settlement for $100,000.

- Your health insurance company puts a hand out and says, "Hey, we paid for that leg surgery. We want our money back out of that settlement."

This is called a lien.

It sounds unfair since you paid your premiums, why do you have to pay them back?

But it’s standard in almost every policy.

It sounds unfair since you paid your premiums, why do you have to pay them back?

But it’s standard in almost every policy.

Where a Lawyer Adds Value:

We don’t just fight the other driver; we negotiate with your health insurance company. If they want $50,000 back, we argue Texas law to try and reduce that number.

Sometimes by huge margins

So more of the settlement money stays in your pocket, not theirs.

Sometimes by huge margins

So more of the settlement money stays in your pocket, not theirs.

What If You Have No Insurance at All? (Letters of Protection)

This is a common scenario in Austin, especially for service industry workers or freelancers. You are hurt, you have no health insurance, and you have no PIP.

You are in pain, but you are scared to go to the doctor because you can’t pay the deductible.

In this case, we use something called a Letter of Protection (LOP).

We send you to doctors who agree to treat you now and get paid later. The LOP is a contract between you, your lawyer, and the doctor. It basically says: "Please fix my client’s back. When we win the case against the bad driver, we promise to pay you out of the settlement funds."

This allows you to get the MRI, the physical therapy, or even the surgery you need immediately, without paying a dime upfront.

What you should remember

The hospital doesn't care about justice; they care about billing cycles.

If you ignore the bills because "it's the other guy's fault," the bills will go to collections. Your credit will tank. And the stress will make your recovery harder.

Use your PIP. Use your health insurance. And let us handle the fight about who pays whom back at the end. Your only job right now is to heal.

Need Legal Help?

Contact our experienced Austin personal injury attorneys for a free consultation.