The App Off Gap in Rideshare Accidents and Insurance Coverage in Texas

Rideshare services like Uber and Lyft are part of everyday transportation across Austin and throughout Texas. While many people assume rideshare accidents are always covered by large corporate insurance policies, that is not always the case.

One of the most confusing situations is known as the app off gap.

The app off gap refers to a period when a rideshare driver is using their personal vehicle but is not logged into the rideshare app. If a crash happens during this time, insurance coverage can become unclear and disputes are common.

Understanding how this gap works is important for injured passengers, other drivers, pedestrians, and even rideshare drivers themselves.

What Is the App Off Gap in Rideshare Accidents

The app off gap occurs when a rideshare driver is not actively using the Uber or Lyft app. This typically includes times when the driver is driving for personal reasons, commuting, or taking a break.

During this period, the rideshare company usually considers the driver a private individual rather than a commercial driver. As a result, the company insurance policies that apply during active rideshare use generally do not apply.

If a collision occurs while the app is off, the rideshare company may deny coverage entirely.

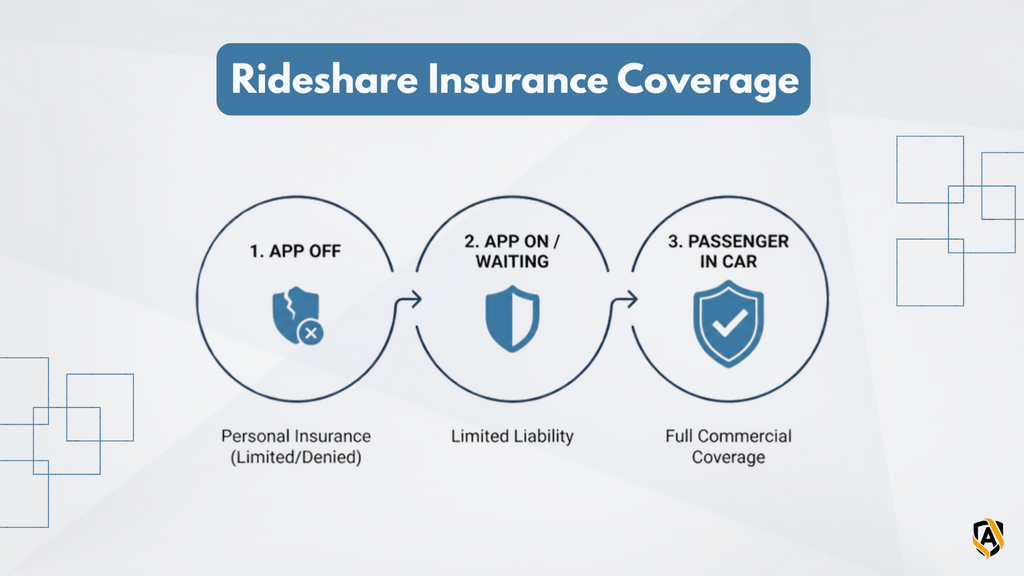

How Rideshare Insurance Typically Works in Texas

Rideshare insurance coverage depends on the driver status at the time of the crash. In Texas, coverage generally falls into three categories.

When the app is off, the driver personal auto insurance is expected to apply. When the app is on but no ride has been accepted, limited rideshare liability coverage may apply. When a ride is accepted or a passenger is in the vehicle, higher commercial coverage limits typically apply.

The app off gap exists entirely outside the rideshare insurance system. This is what makes these cases especially difficult.

For more context on insurance coverage, see Austin rideshare accidents including Uber and Lyft crashes on 6th Street.

Why the App Off Gap Creates Coverage Problems

Many personal auto insurance policies exclude coverage for commercial driving activities, as explained by the Insurance Information Institute (III). Even if the driver was technically off the app, insurers may argue the vehicle was being used in connection with rideshare work.

At the same time, Uber or Lyft may deny responsibility because the driver was not logged in. This can leave injured people caught between insurance companies that each deny responsibility.

In some cases, coverage disputes delay claims, reduce available compensation, or require legal action to resolve.

Who May Be Affected by the App Off Gap

The app off gap can affect several groups of people. Other drivers involved in a crash with a rideshare vehicle may struggle to identify which insurer is responsible. Pedestrians and cyclists may face similar issues.

Passengers who believed they were in a rideshare related situation may later discover the app was not active. Rideshare drivers themselves may find their personal insurance insufficient to cover serious injuries or property damage. Because Texas follows a fault based system, determining liability and coverage is critical.

Passengers who believed they were in a rideshare related situation may later discover the app was not active. Rideshare drivers themselves may find their personal insurance insufficient to cover serious injuries or property damage. Because Texas follows a fault based system, determining liability and coverage is critical.

Understanding how fault is determined in Texas car accidents provides useful context on liability principles.

Why These Cases Often Require Legal Review

App off gap cases often involve detailed investigation. This may include reviewing app activity logs, insurance policy language, crash reports, and driver statements.

The outcome can depend on small details such as whether the driver had recently logged out, whether they were en route to a rideshare related location, or how insurance exclusions are written.

Without careful analysis, injured parties may accept incorrect coverage decisions or miss potential sources of recovery.

Practical Next Steps After an App Off Rideshare Accident

Anyone injured in a collision involving a rideshare vehicle should document as much information as possible. This includes driver details, insurance information, screenshots if the app status is visible, and witness contact information.

Medical evaluation should be obtained promptly, even if injuries seem minor. Insurance conversations should be handled carefully, as early statements may affect coverage determinations. Understanding who pays medical bills after an Austin car accident is also important.

Similar to Austin uninsured motorist claims in Travis County, app off gap cases may involve disputes over insurance coverage.

The Texas Department of Insurance (TDI) regulates insurance practices in Texas and provides consumer resources.

Frequently Asked Questions

Q: What does app off mean in a rideshare accident

A: "App off means the driver was not logged into the Uber or Lyft app at the time of the crash and was not actively working as a rideshare driver."

Q: Does Uber or Lyft insurance apply if the app is off

A: "Generally no. When the app is off, rideshare company insurance usually does not apply, and the driver personal auto insurance is expected to cover the crash."

Q: Can a personal auto insurer deny coverage during the app off gap

A: "Yes. Some personal policies may argue the vehicle was being used for commercial purposes, even if the app was not active."

Q: How can app status be proven after a crash

A: "App status may be determined through rideshare company records, phone data, driver statements, and time stamped activity logs."

Q: Are app off gap accidents harder to resolve in Texas

A: "They often are. These cases commonly involve insurance disputes, coverage denials, and fact specific investigations that take longer to resolve."

The National Association of Insurance Commissioners (NAIC) provides consumer information on insurance coverage and rideshare-related policies.

About the Author

Aaron B Mickens

For over 25 years, Aaron has fought for justice on behalf of Austin's injured. He is committed to standing up to insurance companies and winning for clients across Central Texas.

View all articles by AaronNeed Legal Help?

Contact our experienced Austin personal injury attorneys for a free consultation.